There is no reason whatsoever to believe that the financial carrying capacity of the US economy—or any other DM economy—has improved since the 1980s. In fact, it has gone the other direction in recent years due to aging demographics, declining competitiveness versus the surging EM economies, dwindling rates of productivity growth and a dramatic increase in the leverage ratio against both public and private incomes.

All of these adverse macro-trends mean that the US economy’s ability to generate growth, incomes and profits has been significantly lessened. Accordingly, since its ability to service debt and equity capital at an honest market rate of return has diminished, the logical expectation would be that the finance ratio to national income would fall.

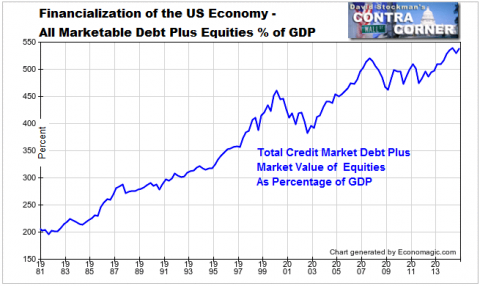

In fact, once Greenspan took the helm and his apparently atavistic embrace of gold standard money melted-down under the Wall Street furies of October 1987, the finance ratio erupted. As shown below, it has never looked back and at 5.5X national income has reached a point that would have been unimaginable on the morning of Black Monday.

Stated differently, under a regime of honest money and market determined financial prices, the combined value of corporate equities and credit market debt would not have mushroomed by 8X—- from $11 trillion to $93 trillion—- during the past 27 years. For crying out loud, the nominal GDP grew by only 3.5X during the identical span. In effect, the US economy has been capitalized at higher and higher rates for no ascertainable reason of fundamental economics.

Indeed, there is no reason why the 260% ratio of equity and credit market debt to GDP that was recorded in 1986 should have risen at all. At that point Paul Volcker had completed his historic task of extinguishing runaway commodity and CPI inflation and had superintended a solid recovery of real economic growth.

Arguably, therefore, the US economy was carrying about the right amount of finance. And, at that healthy ratio, today’s $17.7 trillion economy would be carrying about $43 trillion of combined market equity and credit market debt.

In a word, the Greenspan era of central bank driven price falsification and monetization of trillions of existing assets with credits conjured from thin air has generated a $50 trillion overhang of excess financialization. And that’s just for the US economy. In fact, the central bank error is global and the worldwide excess financialization is orders of magnitude larger.

Total Marketable Securities % of GDP – Click to enlarge

To be sure, the Keynesian economists and power-seeking apparatchik who run the Fed do not openly admit to a massive falsification of financial prices and to responsibility for generating what amounts to a $50 trillion bubble in the US alone.

That’s because they are narrowly and mechanically focused on an altogether different, but impossible task. Namely, guiding the $18 trillion US economy to its full-employment potential. So doing, it pursues its so-called Humphrey-Hawkins “dual mandate” in a manner consistent with the strictures of its Keynesian DSGE (dynamic stochastic general equilibrium) model representation of the US economy.

No comments:

Post a Comment